UK Tax Rates & Allowances (2024/25 & 2025/26)

A clear breakdown of income tax bands, Personal Allowance rules, and key thresholds—so you can plan confidently and avoid surprises.

Blog 05

UK Tax Rates, Thresholds, and Allowances Explained (2024/25 and 2025/26)

The UK tax system is built around a wide range of tax rates, bands, and allowances—and as a business owner or self-employed individual, many of these directly affect how much tax you pay.

Each tax year, the government reviews income tax thresholds, allowances, and reliefs. While not all figures change every year, even small adjustments can have a meaningful impact on your take-home pay and tax planning.

This guide explains the key personal tax allowances and income tax bands for the 2024/25 and 2025/26 tax years, how they work in practice, and where people commonly miss opportunities to reduce their tax bill. For a broader overview of the entire UK tax system, our plain-English guide to how tax works in the UK is a useful starting point.

Why Tax Thresholds Matter More Than You Think

Understanding tax rates alone isn’t enough. Your overall tax position is shaped by:

- Income thresholds

- Tax-free allowances

- Where you live in the UK

- The type of income you earn

These factors interact in ways that can either increase or reduce your tax bill—sometimes unexpectedly.

The government publishes confirmed rates and allowances on Gov.uk before each new tax year begins. Keeping up with these changes allows you to plan proactively rather than react later.

A Quick Note on Regional Differences in the UK

Income tax works slightly differently depending on where you live:

- England and Northern Ireland share the same income tax rates and thresholds

- Scotland sets its own income tax bands and rates

- Wales currently uses the same rates as England and Northern Ireland

The figures below apply to England and Northern Ireland for the 2024/25 and 2025/26 tax years.

The Personal Allowance: Your Tax-Free Starting Point

What Is the Personal Allowance?

The Personal Allowance is the amount you can earn each tax year before you start paying Income Tax. Tax years run from 6 April to 5 April.

For employees, this allowance is applied automatically through PAYE. For the self-employed, it’s accounted for when you submit your Self Assessment tax return.

Personal Allowance for 2024/25 and 2025/26

| Tax Year | Personal Allowance |

|---|---|

| 2024/25 | £12,570 |

| 2025/26 | £12,570 |

When the Personal Allowance Reduces

If your income exceeds £100,000, your Personal Allowance is reduced by £1 for every £2 earned above this level.

Once income reaches £125,140, the allowance is completely removed—creating a high effective tax rate and making planning especially important for higher earners.

How the Personal Allowance Works for Different People

Sole Traders and Freelancers

Your Personal Allowance is applied automatically when HMRC calculates your tax bill after your Self Assessment tax return is submitted.

Limited Company Directors

Directors often structure salary and dividends around the Personal Allowance to maximise tax efficiency. Payroll software usually applies this automatically.

Other Key Personal Allowances to Know About

Trading Allowance and Property Allowance

Two additional £1,000 annual allowances may apply:

- Trading Allowance – small amounts of self-employed income

- Property Allowance – small amounts of rental income

These allowances are not available for income earned through a limited company and can simplify reporting where income is modest.

Personal Savings Allowance (PSA)

| Taxpayer Type | PSA |

|---|---|

| Basic rate | £1,000 |

| Higher rate | £500 |

| Additional rate | £0 |

If your income is below £12,570, you may also qualify for the starting rate for savings, allowing up to £5,000 of interest to be tax-free.

Marriage Allowance

Marriage Allowance allows one partner to transfer part of their unused Personal Allowance to the other.

You may be eligible if:

- One partner earns below £12,570

- The other is a basic-rate taxpayer

Up to £1,260 can be transferred for both tax years. HMRC adjusts the recipient’s tax code automatically once claimed.

Blind Person’s Allowance

| Tax Year | Allowance |

|---|---|

| 2024/25 | £3,070 |

| 2025/26 | £3,130 |

This is added on top of the Personal Allowance and may be transferred to a spouse or civil partner if unused.

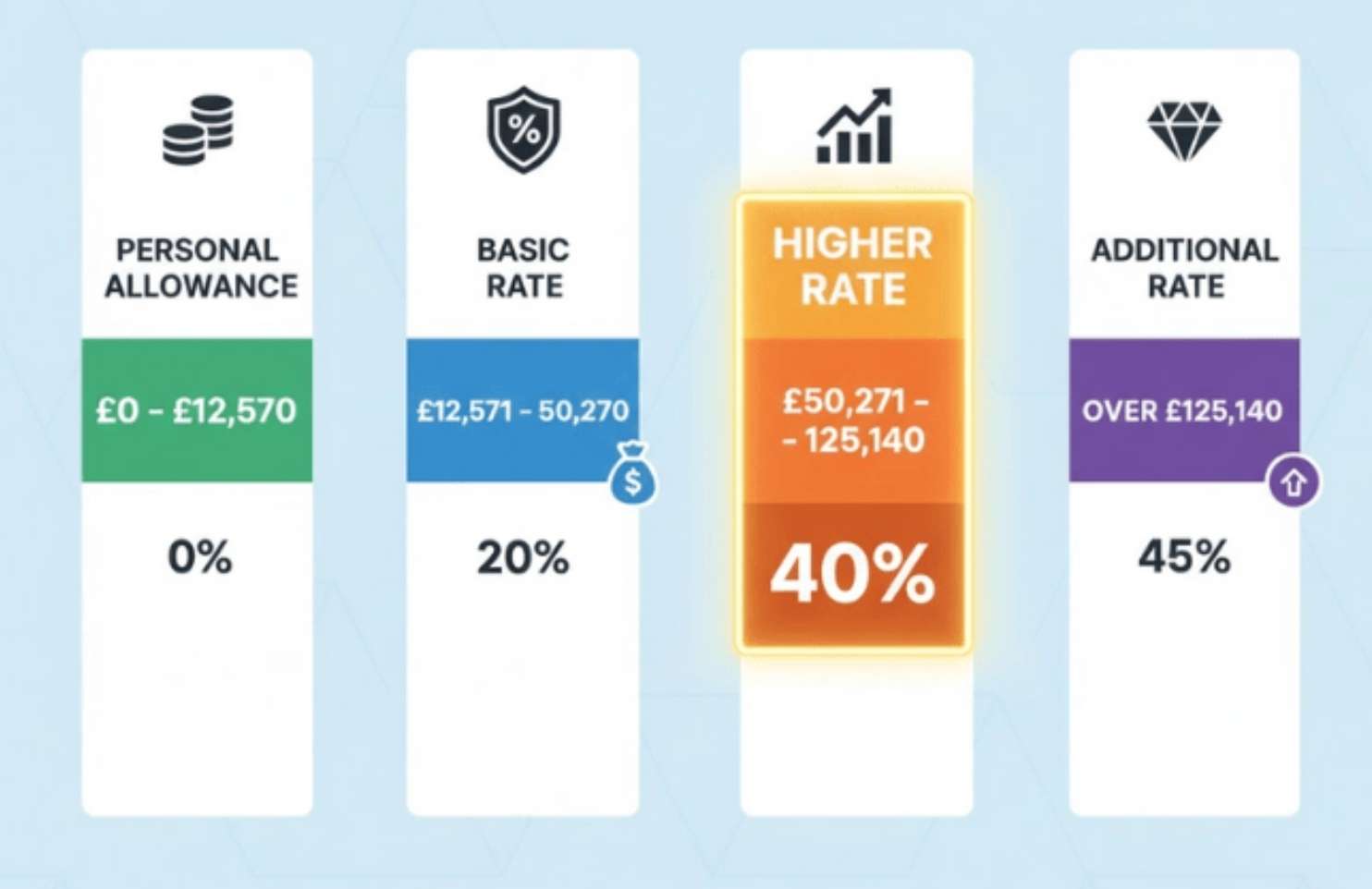

Income Tax Bands and Rates (England & Northern Ireland)

Income tax is marginal, meaning only income within each band is taxed at that rate.

| Tax Band | Income Range | Rate |

|---|---|---|

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

Pension contributions and Gift Aid donations can reduce income subject to higher rates. For a full range of strategies, our guide on how to pay less tax in the UK legally explains each approach in detail.

High Income Child Benefit Charge (HICBC)

If you or your partner receive Child Benefit:

- The charge starts when income exceeds £60,000

- Benefit is reduced by 1% for every £200 between £60,000 and £80,000

- At £80,000, Child Benefit is fully repaid

This is based on individual income, not household income.

Why Understanding These Rules Matters

It’s also worth knowing the key filing and payment dates. Our Self Assessment deadlines guide and UK tax dates and deadlines page cover all the important dates throughout the year.

Understanding how allowances and thresholds interact can help you:

- Avoid unnecessary higher-rate tax

- Protect your Personal Allowance

- Reduce exposure to HICBC

- Plan salary, dividends, and pensions more effectively

Final Thoughts

Tax doesn’t have to be overwhelming, but it does reward attention and planning.

Whether you’re employed, self-employed, or running a limited company, understanding UK tax rates and allowances puts you in control—helping you stay compliant, minimise surprises, and make confident financial decisions year after year. If you’d like tailored support, contact SRZ Accountancy—our accountants work with sole traders, landlords, and limited companies across the UK.

Book your free consultation

The best way to find out how we can help is a quick conversation. Tell us about your situation — your goals, your challenges, your current accountancy needs. The first meeting is always free, with no obligation and no sales pressure.